Income Tax and Instructions for e-Filing

Income Tax is a direct tax that is charged on an Assessee’s income. The tax is calculated on the net taxable income of the assesse according to the applicable slab rate as prescribed in the finance Act applicable for the year.

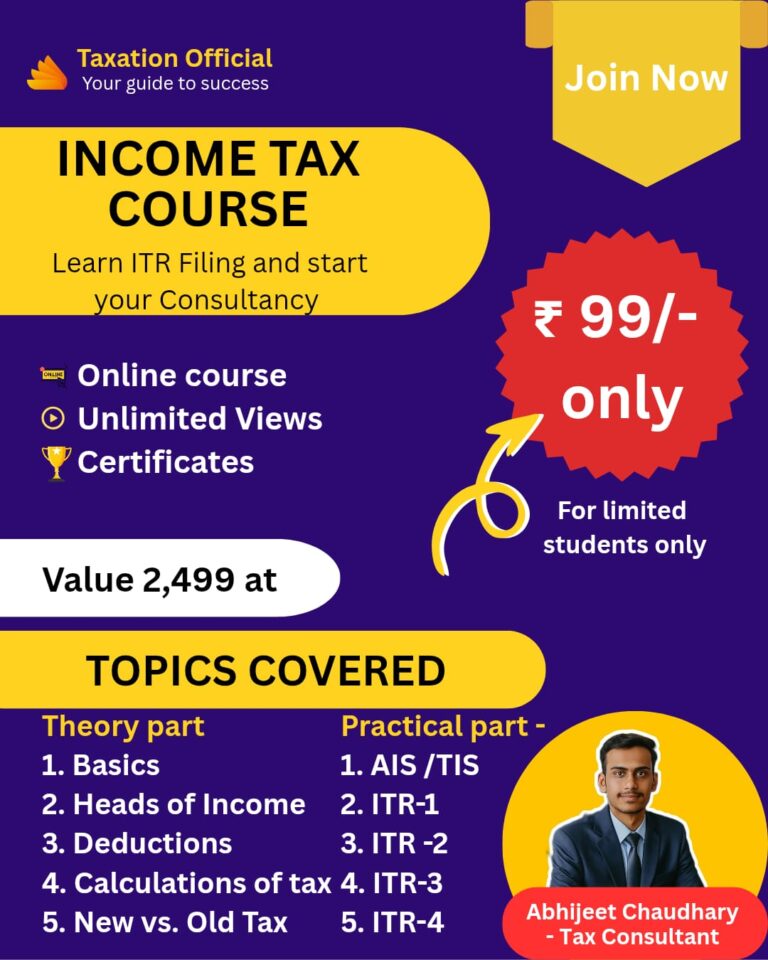

Note: You can now file your taxes through the New income tax portal. The New portal has many features and is designed to ease the tax filing process. For ITR filing watch our complete video on our website in course section.

In the Union Budget 2023, announced on 1 February 2023, the Finance Minister announced specific revisions to the tax slabs and tax rates, which are summarized in this article

What is Income Tax?

Income tax is a tax charged on the annual income earned by an Assessee. The amount of tax paid will depend on how much money you make as income in the previous year.

Previous year the year in which income is earned and Assessment year the which tax is to be paid. Usually assessment year is next year , as we have to pay tax in next year on income earned in last year. However, in some cases tax is liable to be paid in the same year, those are special cases.

One can proceed with Income tax payment, TDS/TCS payment, and Non-TDS/TCS payments online. All taxpayers must fill in the relevant details to make these payments. The entire process becomes simple and quick.

Recent Updates on Income Tax

FY 2023-24 Income tax applies to all residents whose annual income exceeds Rs.3 lakh p.a. The highest amount of tax an individual could pay is 30% of their income plus cess at 4% if their income is more than Rs.15 lakh p.a.

Under the new tax regime, the rebate for income tax has been increased to Rs.7 lakh from the earlier limit of up to Rs.5 lakh, while the surcharge rate on income of Rs.5 crore and above has been decreased from 37% to 25%.

Who Should Pay Income Tax?

It is mandatory to file ITR for individuals If the total Gross Income is over Rs.3,00,000 in a financial year (Including standard deduction). This limit exceeds Rs.3,00,000 for senior citizens and Rs.5,00,000 for super senior citizens. The assessee listed below must pay taxes and file their income tax returns.

1. Artificial Judicial Persons

2. Corporate firms

3. Association of Persons (AOPs)

4. Hindu Undivided Families (HUFs)

5. Companies

6. Local Authorities

7. Body of Individuals (BOIs)

Who are Taxpayers?

An Individuals who are above 60 years of age and earn over Rs.2.5 lakhs yearly should pay taxes to the Indian Government.

Types of Income Based on Income Tax Criteria

An individual in India who earns or receives a regular source of income is subject to income tax. The Revenue Tax Department has segmented income into five different categories:

• Property Income – Renting a house is taxable under this type of income.

• Salary Income – Income earned as a salary or pension is also taxable under this type of income.

• Business or Professional Income – Profits generated by self-employed individuals, freelancers, businesses, or contractors, and income made by professionals like chartered accountants, life insurance agents, lawyers, and doctors who practice in their fields, including tuition teachers, are taxable under this type of tax.

• Capital Gain Income – Surplus income generated from the sale of capital assets like stocks, mutual funds, or real estate is taxable under this type of income.

• Income from Other Sources – Income earned as interest from savings bank account, fixed deposits, and lottery winning are considered as income from other sources.

Taxpayers and Income Tax Slab Rates

In the Union Budget 2023, the Finance Minister of India announced a new income tax slab. However, the new income tax regime is optional, and individuals can opt for it or file their taxes as per the old regime.

Income Tax slab under New Regime for FY 2023-24

Income Tax Slab Tax Rate

Up to Rs.3 lakh Nil

Above Rs.3 lakh – Rs.6 lakh 5%

Above Rs.6 lakh – Rs.9 lakh 10%

Above Rs.9 lakh – Rs.12 lakh 15%

Above Rs.12 lakh – Rs.15 lakh 20%

Above Rs.15 lakh 30%

Note: New income tax rates are optional

Join Our latest course …

Income Tax Slab (Old Regime) for individuals who are less than 60 years old

Income Tax Slab Tax Rate

Up to Rs.2,50,000 Nil

From Rs.2,50,001 to Rs.5,00,000 5%

From Rs.5,00,001 to Rs.10,00,000 20% of the amount exceeding Rs.5 lakh

More than Rs.10,00,000 30% of the amount exceeding Rs.10 lakh

*An additional cess of 4% will apply to the tax amount calculated above.

Depending on the age of the individual, the three categories that individual resident taxpayers are divided into are mentioned below

• Individuals who are less than the age of 60 years old.

• Senior citizens who are above 60 and below 80 years of age.

• Super senior citizens who are above 80 years old

Senior and Super Senior Citizens Income Tax Slabs (Old Regime) as Follows:

|

Income Tax Slabs |

Rates (above 60 years &below 80 years ) |

Rates (above 80 years) |

|

Up to Rs.3,00,000 |

NIL |

– |

|

upto Rs.5,00,000 |

10% |

NIL

|

|

From Rs.5,00,001 to Rs.10,00,000 |

10% |

20% |

|

More than Rs.10,00,000 |

30% |

20% |

Advance Tax

Calculating tax liability beforehand and paying the taxes to the government accordingly is called advance tax. There are specific deadlines for the advance tax payments. These deadlines are listed below:

|

Due Date |

Advance Tax Payable |

|

On or before 15 June |

15% of advance tax |

|

On or before 15 September |

45% of advance tax |

|

On or before 15 December |

75% of advance tax |

|

On or before 15 March |

100% of advance tax |

Income Tax Return

Here is all you need to know about how to file ITR online. Before you file your taxes, you will need your Form 16, provided by your employer, and any proof of investment. You can compute the tax payable and any refunds for the year. You can download the IT preparation software from the IT department’s website. Once you have all the documents ready, you can start the Income tax return filing process.

For MSMEs and professionals, the next-generation common IT form has been introduced; if their cash receipts are less than 5%, presumptive tax limitations have been raised to Rs 3 crore (turnover) and Rs 75 lakh (income).

E-Filing Income Tax

E-Filing Income Tax Returns, TDS returns, AIR returns, and Wealth Tax Returns can be completed online at https://incometaxindiaefiling.gov.in.

E-filing your return has apparent advantages like you won’t have to deal with the hassle of paperwork and waste time sorting through it all. You can log on to the secure website and e-file your return.

This government website also has provisions for you to submit returns, view form 26AS, outstanding tax demand, CPC refund status, rectification status, ITR – V receipt status, online application tools for PAN and TAN, e-pay your tax and even has tax calculator.

Income Tax Calculation

Income tax calculation can be done manually or using an online income tax calculator. The amount of tax that must be paid will depend on the tax slab under which you fall. A salaried employee’s income includes basic pay, House Rent Allowance (HRA), Transport Allowance, Special Allowance, and other allowances.

However, specific components of your salary are tax-exempt, like Leave Travel Allowance (LTA), reimbursement of telephone bills, etc. If HRA is part of your salary and you reside in a rented house, you can claim an exemption. Apart from these exemptions, there is a standard deduction of up to Rs.50,000.

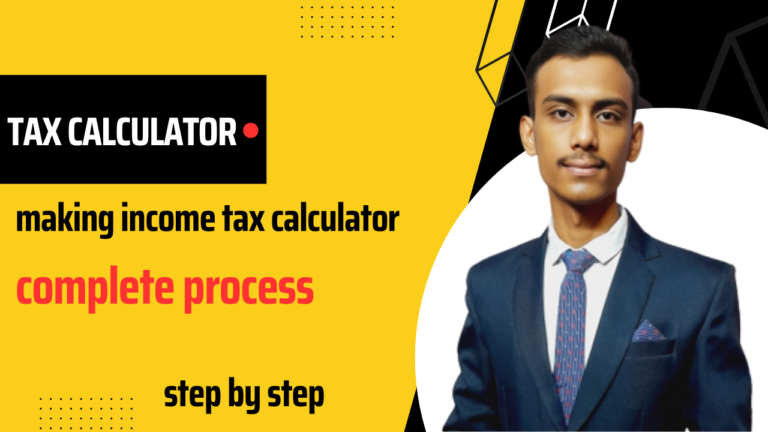

Online Tax Calculator – watch our video on how to make tax calculator on our website course section

Important Income Tax Dates 2023

The important dates to remember in FY 2023 –24 are mentioned in the table below:

|

Important Dates |

Task Must be Completed |

|

Before 31 January |

Individuals must submit their proof of investment |

|

Before June 31 |

Link Aadhaar to PAN |

|

Before July 31 not |

Due date to file ITR by Individual / HUF/ AOP/ BOI (books of accounts

|

|

|

required to be audited) |

|

Before October 31 |

Due date to file ITR by Businesses (Requiring Audit) |

|

Before November 30 |

Due date to file ITR by Business firms requiring TP report |

|

Before December 31 |

Due date to file Revised/Belated ITR |

Income Tax Payment Details

Taxpayers can pay taxes online by using the e-Payment facility. To avail online tax payment facility, taxpayers must have a net-banking account with an authorized bank. The Permanent Account Number (PAN) or Tax Deduction and Collection Number (TAN) will also have to be provided for validation.

About Income Tax Department India

A government agency that undertakes the direct collection of tax in India is the Income Tax Department. All operations of the department are handled by the Central Board for Direct Taxes (CBDT). Individuals can get details such as international taxation, tax laws and rules, organizational setup, etc., on the official website of the department.

Income Tax Act

Passed in 1961, the Income Tax Act of India handles all income tax provisions as well as any tax deductions that may be applicable. Since its introduction, there have been many changes to the law because of economic situations and inflation.

Income Tax Rules in India

The legislature enacted the Income Tax Act of 1961 to administer and govern income tax in the country. Still, the Income Tax Rules, 1962, were created to help in applying and enforcing the law constituted in the Act. Moreover, the Income Tax Rules can only be read with the Income Tax Act.

The Income Tax Rules are within the framework of the Income Tax Act and are not allowed to override its provisions.

Income Tax Collection (reference form government public announcements)

The government collects taxes in three primary ways:

1. Voluntary taxpayer payments into designated banks, like Advance tax & self-assessment tax.

2. Taxes Deducted at Source (TDS) which is deducted from your monthly salary before you receive it.

3. Taxes Collected at Source (TCS).

Under the Department of Revenue of the Ministry of Finance, the Income Tax Department (IT Department) handles monitoring the collection of Income Tax, Expenditure Tax, and various other Financial Acts that are passed every year in the Union Budget.

The Central Board of Direct Taxes (CBDT) regulates the policy and planning of taxes. CBDT is also responsible for administering direct tax laws through the IT Department.

Besides collecting taxes, the IT department is also involved in preventing and detecting tax avoidance.

Income Tax Form Numbers

If an assessee wants to claim an income tax refund, they must first file the income tax return. Depending on the income assessment group, the individual will need to submit one of the ITR forms listed below:

Types of ITR Forms :

ITR-1 = Individuals with Income from Salaries, One house property, other sources (Interest etc.)

ITR-2 = For Individuals and HUFs not having Income from Business or Profession

ITR-2A = For Individuals and HUFs not having Income from Business or Profession and Capital Gains and who do not hold foreign assets

ITR-3 = For Individuals/HUFs being partners in firms and not carrying out business or profession under any proprietorship

ITR-4 = For individuals and HUFs having income from a proprietary business or profession

ITR-4S = Presumptive business income tax return

ITR-5 = For persons other than, – (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7

ITR-6 = For Companies other than companies claiming exemption under Section 11

ITR-7 = For persons including companies required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) or 139(4E) or 139(4F)

ITR-V = The acknowledgment form of filing a return of income

To file the ITR, an individual must produce the bank statement, Form 16, and a copy of the previous year’s returns. To register and file the returns, the individual must visit the Income Tax Department’s website – https://incometaxindiaefiling.gov.in/.

Income Tax Refund FY 2023-24

If you have paid more tax than your actual tax liability, you can claim an income tax refund of the extra money you have paid.

For example, if your TDS liability for FY 2023-2024 was Rs.35,000 and your employer deducted Rs.40,000 instead, you can claim a refund for the additional Rs.5,000 that was deducted.

You can also claim an income tax refund in case you forgot to declare your tax-saving investments and tax has been charged to you without considering your deductions. Individuals can check income tax refund status on the official website of Income Tax Department.

Income Tax Saving Investments

Declaring investments – From HRA, Life Insurance Premiums, National Savings Certificate, Leave Travel Allowance to Fixed Deposit (minimum of 5 years), ELSS Tax Saving Mutual Funds, and more, by ensuring that you have declared all your investments, you can achieve more deductions on tax. The following options can be considered for saving on income tax.

Investment options

Mutual funds such as Equity Linked Savings Schemes (ELSS) can be claimed for tax deduction under Section 80C. Compared to fixed deposits and PPFs, the ELSS offers a shorter lock-in period and more benefits when making money.

Unit Linked Insurance Plans (ULIP) are insurance schemes linked to the market. The investment made under ULIP qualifies for tax deductions.

Insurance

Life Insurance and Health Insurance – The money paid towards life insurance and health insurance policies is considered for tax deductions under Section 80C.

Home Loans

When we take a loan for buying a house or for renovation purposes, we are eligible for tax deductions up to Rs.1.5 lakh for a financial year. However, there are no tax exemptions allowed on personal loans.

You can also consider the following options for reducing tax amount on your income.

• Fixed Deposits (FD) – An FD with a lock-in period of five years can help you save on tax while earning interest on the deposited amount.

• National Saving Certificate (NSC) – The NSC offers a safe and reliable investment method. You can deposit as low as Rs.100 for a 5-10 year lock-in period. The investments made under NSC are eligible for tax deductions.

• Provident Fund (PF) – You can also choose to invest more towards your PF account, which will help you reduce your taxable amount.

Income Tax Deduction Section details

Deductions for your taxable amount are available under various sections of the Income Tax Act 1961. Deductions must be mentioned in the appropriate ITR form when e-filing income tax returns.

• Section 80C: Deductions under this section are only available to individuals and HUF. This section allows certain investments like NSC, etc. and expenditures to be exempt from taxation up to Rs.1.5 lakh.

• Section 80CCC: Deductions under this section are on payments made to LIC or any other approved insurance company under an approved pension plan. The pension policy must be up to Rs.1.5 lakh and be taken for the individual himself out of the taxable income.

• Section 80CCD: Deductions under this section are for contributions to the New Pension Scheme by the assessee and the employer. The deduction equals the contribution, not exceeding 10% of his salary. The total deduction available under Section 80C, 80CCC and 80CCD is Rs.1.5 lakh. However, contributions to the Notified Pension Scheme under Section 80CCD are not considered in the Rs.1.5 lakh limit.

• Section 80D: This is the section that deals with income tax deductions on health insurance premiums paid. In the case of individuals, the insurance policy can be taken to cover himself, his spouse, dependent children – for up to Rs.15,000 and parents (whether dependent or not) – for up to Rs.15,000.

An additional deduction of Rs.5,000 is applicable if the insured is a senior citizen. In the case of HUF, any member can be insured, and the general deduction will be for up to Rs.15,000 and an additional deduction of Rs.5,000.A total of Rs.2.0 lakh can be claimed as deductions whether the assessee is an individual or a HUF.

• Section 80DDB: This section is for deductions on medical expenses that arise for treatment of a disease or ailment as specified in the rules (11DD) for the assessee, a family member or any member of a HUF.

• Section 80E: This section deals with the deductions applicable to the interest paid on education loans for education in India.

• Section 80EE: This section deals with tax savings applicable to first-time homeowners. Section 80EE applies to individuals whose first home purchased has a value less than Rs.40 lakh and the loan taken for Rs.25 lakh or less.

• Section 80RRB: Deductions with respect to income by way of royalties or patents can be claimed under this section. Income tax can be saved up to Rs.3.0 lakh for patents registered under the Patents Act 1970.

• Section 80TTA: This section deals with the tax savings applicable on interest earned in savings bank accounts, post offices or cooperative societies. Individuals and HUFs can claim a deduction on an interest income of up to Rs.10,000.

• Section 80U: This section deals with the flat deduction on income tax that applies to disabled people when they produce their disability certificate. Up to Rs. 1.0 lakh can be non-taxed, depending on the severity of the disability.

• Section 24: This section deals with the interest paid on housing loans that are exempt from taxation. An amount of up to Rs.2.0 lakh can be claimed as deductions per year, in addition to the deductions under Sections 80C, 80CCF and 80D. This is only for self-occupied properties. Properties rented out, 30% of rent received, and municipal taxes paid are eligible for tax exemption.

No matter if some one searches for his essential thing,

thus he/she needs to be available that in detail, so that

thing is maintained over here.